ITG Opt

Advanced portfolio construction, optimization, hedging, and refinement

Highlights

- Fast mixed-integer programming solver that handles complex problems with various integer constraints on thousands of securities such as turnover, round lot size, position count, minimum trade size, and threshold position size

- Nonlinear transaction cost modeling, including turnkey support for ITG’s Cost Curves

- Model taxes to encourage, discourage, and constrain capital gains and losses in each holding period, both in gross and net terms, while avoiding wash sales

- Robust optimization to help reduce the effects of alpha estimation error by incorporating uncertainty measures into the objective function

- Manage a variable set of portfolio strategies, including passive index and ETF tracking, enhanced indexing, active, hedge fund, pension fund, long/short, market neutral, dollar neutral, sector neutral, 130/30, and transition, while incorporating restrictions

Description

ITG Opt™ is a flexible portfolio construction platform. It helps portfolio managers develop new strategies and solve complex, real-world optimization problems that consider nonlinear transaction costs, taxes, leverage, and return forecast uncertainty, in addition to traditional portfolio optimization goals such as risk and return. Given initial holdings, ITG Opt produces an optimal portfolio, various portfolio statistics, and a trade list that can be sent to trading destinations.

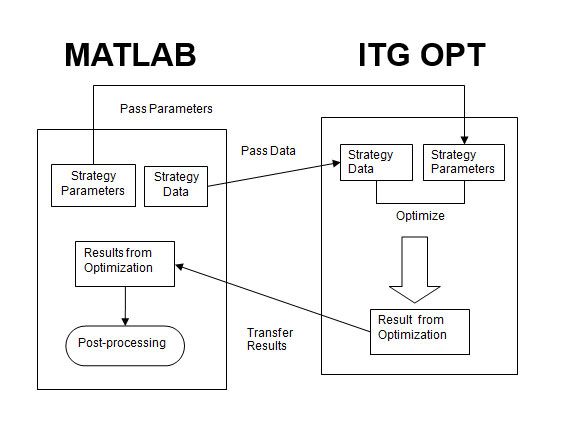

ITG Opt leverages the native Java® interface in MATLAB®, enabling users to pass market data and set optimization strategy parameters with well-documented MATLAB functions.

ITG

One Liberty Plaza

165 Broadway

New York, NY 10006

UNITED STATES

Tel: 866-829-5392

ITG_OPT_SUPPORT@itg.com

https://www.virtu.com/

Required Products

Platforms

- Windows

Support

- Fax

- On-site assistance

- Telephone

- Training

Product Type

- Modeling and Simulation Tools

Tasks

- Data Analysis and Statistics

Industries

- Financial Services

Related Connections Views: Modeling and Simulation Tools, Data Analysis and Statistics, Financial Services